Choosing between a 401(k) and a 403(b) isn’t about picking the “better” plan—it’s about understanding which one you have access to and how to use it effectively. Both are tax-advantaged retirement accounts designed to help you build long-term savings, but they differ in who can use them, how they’re structured, and what options you may have inside the plan. If you’re not sure how much you can realistically contribute, it helps to understand where your money actually goes each month first.

What Is a 401(k)?

A 401(k) is an employer-sponsored retirement plan offered by private-sector companies. If you work for a for-profit business, this is the most common retirement account you’ll encounter.

Key features:

- Contributions are made pre-tax (traditional) or after-tax (Roth option, if offered)

- Employers often provide matching contributions

- Wide range of investment options (mutual funds, index funds, target-date funds)

- Annual contribution limits set by the IRS

What Is a 403(b)?

A 403(b) is similar in structure but is designed for employees of nonprofit organizations, public schools, and certain government entities.

Key features:

- Available to teachers, healthcare workers, and nonprofit employees

- Contributions can be pre-tax or Roth (depending on the plan)

- Often includes annuity-based investment options (in addition to mutual funds)

- May offer additional catch-up contribution rules for long-tenured employees

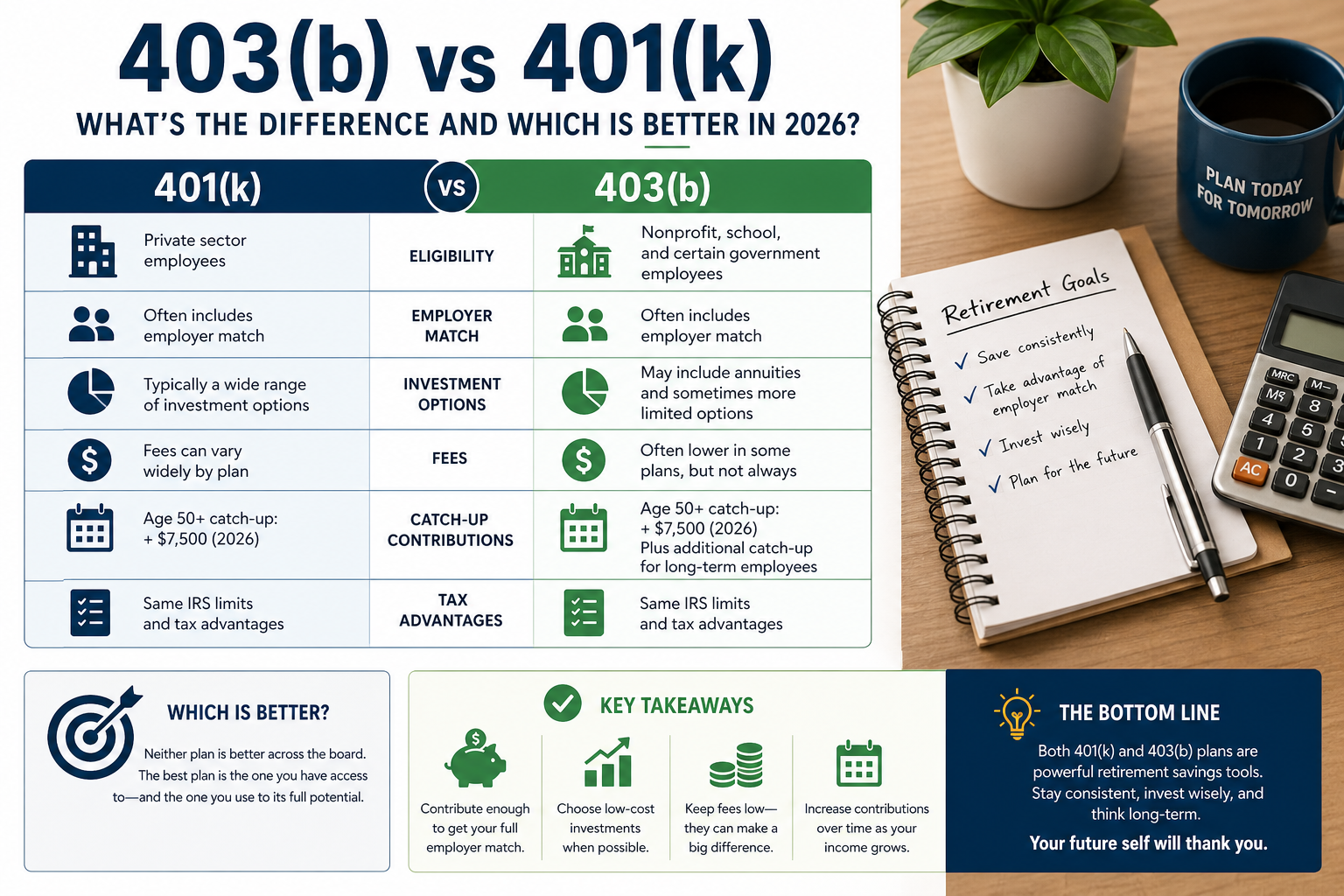

401(k) vs 403(b): Side-by-Side Comparison

| Feature | 401(k) | 403(b) |

|---|---|---|

| Who can use it | Private sector employees | Nonprofits, schools, certain government roles |

| Employer match | Common | Common (varies by employer) |

| Investment options | Typically broad | Sometimes more limited |

| Fees | Can vary widely | Often lower in some cases |

| Catch-up contributions | Age-based | Age-based + long-service option |

Contribution Limits (2026)

Both plans follow the same IRS limits:

- Employee contribution: $23,000

- Age 50+ catch-up: +$7,500

Some 403(b) plans allow an additional catch-up contribution if you’ve worked with the same employer for 15+ years.

Investment Options: What to Expect

401(k)

- Index funds (S&P 500, total market)

- Target-date retirement funds

- Employer stock (in some cases)

403(b)

- Mutual funds

- Annuities (more common here)

- Sometimes fewer low-cost index fund options

Fees: The Hidden Factor

Fees can quietly eat into your retirement savings over time. That’s why reducing unnecessary spending—using strategies like cutting your monthly expenses without sacrificing your lifestyle—can make a bigger impact than most people expect.

- 401(k) plans vary widely depending on the employer and provider

- 403(b) plans sometimes offer lower administrative costs—but not always

Always review:

- Expense ratios

- Administrative fees

- Advisor or management fees

Which One Is Better?

There’s no universal winner. The right move is to optimize the plan you have.

Choose a 401(k) strategy if:

- You have access to strong employer matching

- Your plan includes low-cost index funds

- You want broader investment flexibility

Choose a 403(b) strategy if:

- You qualify for the additional catch-up contributions

- Your plan offers low-fee investment options

- You work long-term in education or nonprofit sectors

How to Decide What to Do Next

- Check your employer match

Always contribute enough to get the full match—it’s effectively free money. - Review your investment options

Look for low-cost index funds whenever possible. - Understand your fees

Even a 1% difference in fees can significantly impact long-term returns. - Increase contributions over time

Gradually raise your contribution rate as your income grows.

The Bottom Line

The difference between a 401(k) and a 403(b) comes down to where you work and how your plan is structured—not which one is inherently better.

Your ability to contribute consistently is often tied to bigger financial decisions, including whether you rent or buy and how much flexibility you have in your budget. What matters most is:

- Contributing consistently

- Taking advantage of employer match

- Keeping fees low

- Staying invested long-term

Do that, and either plan can help you build meaningful retirement savings.